Key Takeaways

In April, lower-income U.S. adults and those with limited-to-no financial assets were more likely to trade down to cheaper substitutes or forgo purchases of consumer goods and services entirely when faced with sticker shock.

However, certain attributes of financial wealth were also tied to stronger responses to inflation in April. Adults with invested assets and those without were almost equally likely to report forgoing purchases when faced with sticker shock; when faced with a similar dilemma, homeowners were more likely than renters to trade down.

Rising prices and financial market volatility are increasingly impacting purchasing decisions and threatening to slow the pace of consumer spending growth going forward.

Earlier this month, Morning Consult released the May 2022 edition of the U.S. Supply Chains & Inflation report. The report examined recent developments in consumer purchasing behavior through a new framework of five indexes tracking price sensitivity, substitutability, unavailability, purchasing difficulty and delivery delays across various goods and services. Here, we supplement the insights from the latest report by taking a closer look at how inflation is differentially impacting U.S. adults based on income and wealth.

Rising incomes are partially insulating consumers from the impacts of inflation

One of the many unique features of the 2020 pandemic recession was the fact that inflation-adjusted personal incomes largely increased during this time (except for March 2020). While this is true only when government transfers are counted in personal incomes, the fact remains that personal savings rates nearly tripled during this period. These values in the aggregate can often obscure important variation across the income distribution, but even in this dimension, it is clear that consumers built up a very large savings buffer over the past two years. Now, with inflation eroding consumer purchasing power, that buffer is being depleted.

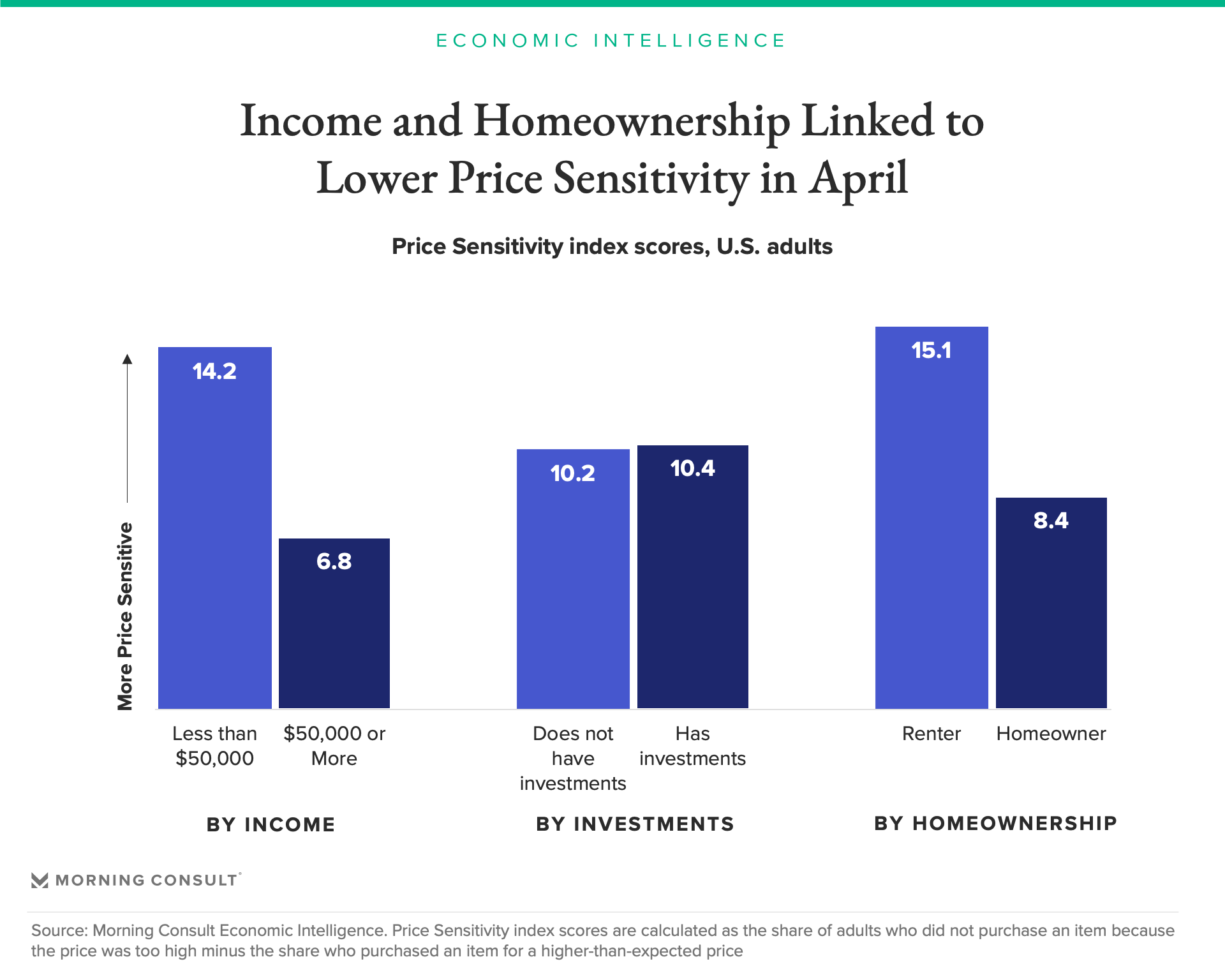

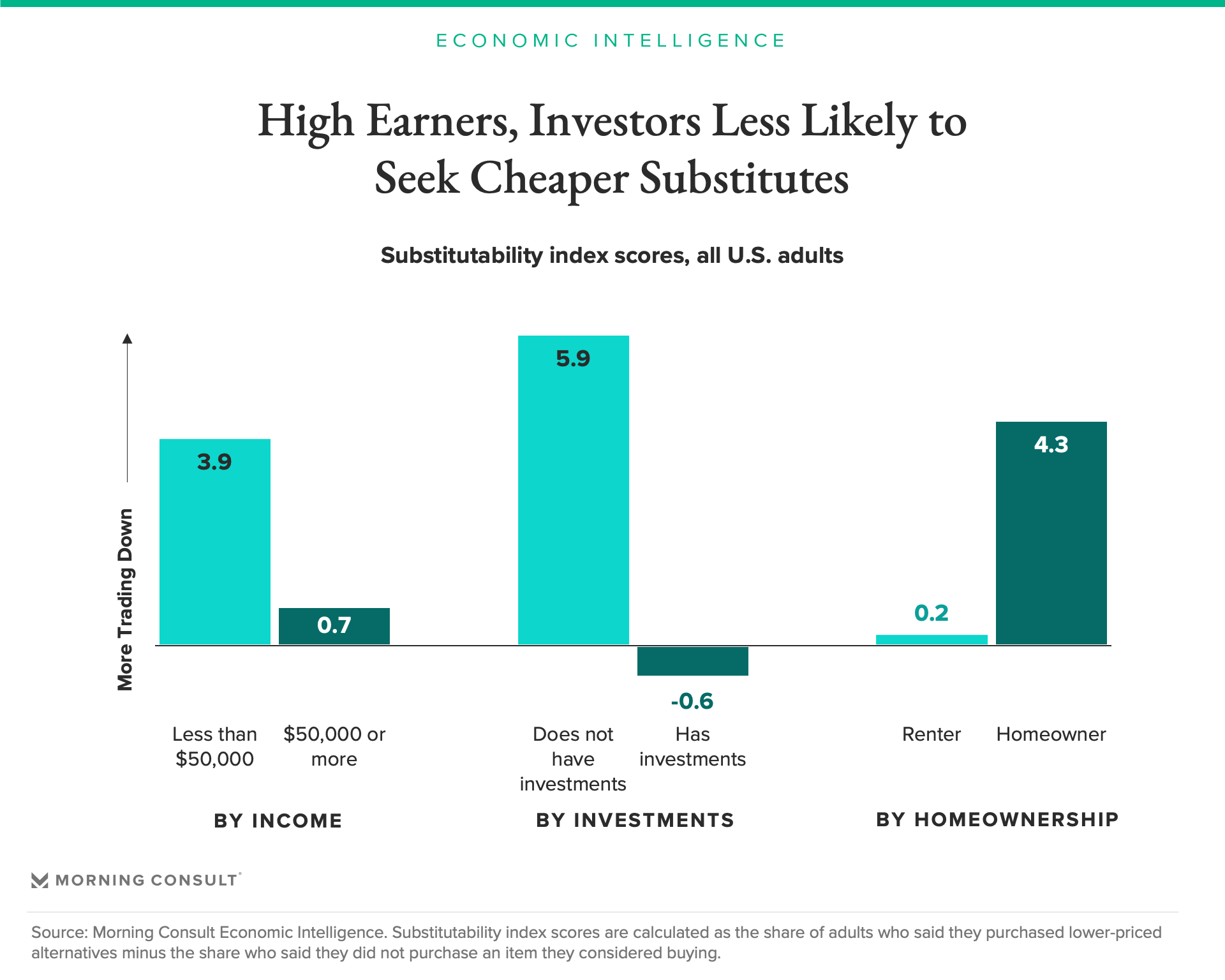

Morning Consult’s newest indexes demonstrate that income inequality is playing an important role in consumers' response to inflation: With inflation tightening its grip on household budgets in April, consumers reported increases in both price sensitivity (measured as the willingness to forgo a purchase when faced with sticker shock) and substitutability (measured as the willingness to trade down to a cheaper substitute).

The spending habits of lower-income adults have been most broadly impacted by inflation. However, the spending habits of high earners have also become increasingly reactive to inflation, with price sensitivity spiking in April for categories ranging from housing and vehicles to gas and personal care.

Higher net worth is also partially insulating consumers from inflation

Income reflects a limited amount of information about consumers' spending power. To better understand the response to inflation from households of varying wealth (as inferred by their asset holdings), we next compare differences in price sensitivity and substitutability among U.S. adults by financial market investments and homeownership status in addition to income.

Overall, higher wealth tended to correspond with less price sensitivity and trading-down behavior in April. Homeowners and adults from households earning at least $50,000 per year had lower scores for the Price Sensitivity and Substitutability indexes than their lower-earning or rent–paying counterparts.

Additionally, adults from higher-income households and those who said they owned investments were less likely to report having opted for cheaper alternatives when purchasing goods and services last month.

These findings make sense: Wealthier households tend to have a larger nest egg to fall back on in times of rising prices, whereas those with a less substantial savings buffer are closer to running out of money if expenses continuously outpace their incomes. More financially vulnerable adults are therefore more likely to defer or cancel discretionary purchases due to high prices, or to trade down to lower-cost alternatives of essential purchases like groceries. In contrast, higher-income households are more likely to adjust their spending on nonessentials. Elements of all of these changes in spending habits can be seen in the full Morning Consult report for May.

Is the tide beginning to turn?

Homeowners and those with invested assets have benefited tremendously over the last two years from rising home and equity prices, experiencing the classic wealth effect supporting their spending habits. There are signs, however, in the Morning Consult data that this may be changing based on recent stock market declines. In April, adults with investments — typically an indication of higher wealth — exhibited slightly higher price sensitivity than adults with no investments. Although invested assets are not necessarily liquid, they imply some manner of safety net, akin to a savings buffer, for adults who have them. Consumers watching their stock market portfolios shrink are finding themselves less well off than they expected, and act accordingly in their spending.

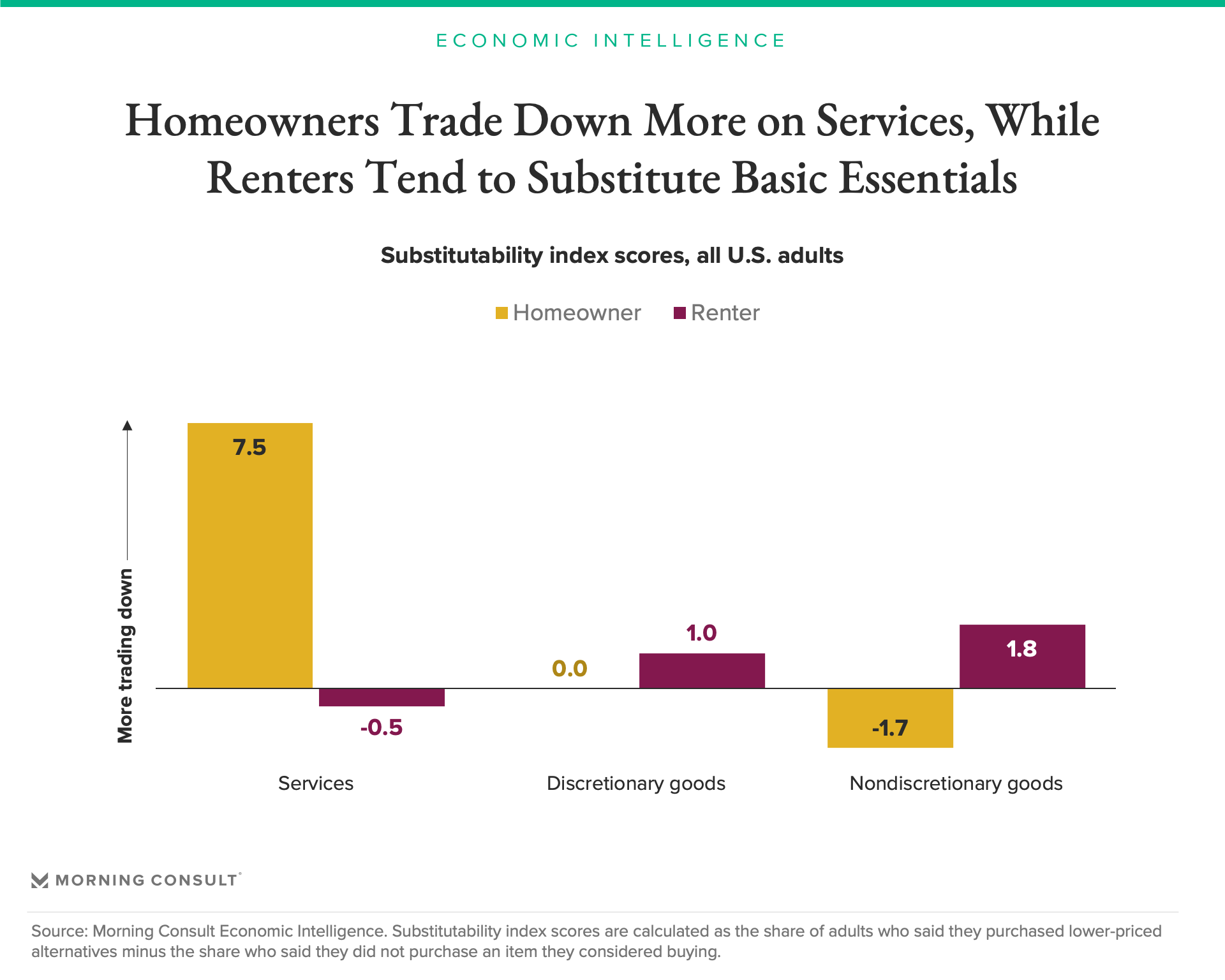

The impact of inflation on purchasing behavior seems to be manifesting itself a little differently in the housing market: Homeowners showed a higher inclination to trade down than renters did last month. Much of this difference was driven by services — particularly housing, which is categorized as a service since it fulfills the need for shelter. Rising home prices and interest rates have made homebuying increasingly unaffordable.

In addition to home values, which are making down payments harder to afford, the growing cost burden from higher mortgage rates may be forcing prospective buyers to opt for lower-priced homes than they originally sought. Renters, meanwhile, were more likely to trade down on essential goods like groceries or personal care items.

Mounting threats to consumer spending

The outlook for the U.S. consumer is becoming increasingly cloudy. Declining stock market prices, rising debt utilization, and the persistent gap between household income growth and inflation all point to consumers who are being forced to spend down their pandemic savings. With inflation now also beginning to encroach on broader spending habits, per the latest data from Morning Consult, inflation-adjusted consumer spending growth is likely to continue to slow.

Kayla Bruun is the lead economist at decision intelligence company Morning Consult, where she works on descriptive and predictive analysis that leverages Morning Consult’s proprietary high-frequency economic data. Prior to joining Morning Consult, Kayla was a key member of the corporate strategy team at telecommunications company SES, where she produced market intelligence and industry analysis of mobility markets.

Kayla also served as an economist at IHS Markit, where she covered global services industries, provided price forecasts, produced written analyses and served as a subject-matter expert on client-facing consulting projects. Kayla earned a bachelor’s degree in economics from Emory University and an MBA with a certificate in nonmarket strategy from Georgetown University’s McDonough School of Business. For speaking opportunities and booking requests, please email [email protected]

Scott Brave previously worked at Morning Consult in economic analysis.